In this article and the slideshow below, we invite you to (re)discover key concepts such as property donation, usufruct rights, and the right of residence, helping you make informed decisions and potentially save substantial amounts — at least 36%! Acting early is highly advantageous, especially since usufruct and residence rights allow you to continue enjoying your property.

Of course, this isn’t always possible due to mortgage constraints. When a mortgage exists, it can be transferred to the beneficiary of the donation, provided they can assume the payments. The outstanding debt is then deducted from the property’s value when calculating the donation tax. The mortgage can also be increased — within affordability limits — to optimize the donation from a tax perspective and leave liquidity to the donor.

A donation to your descendants can be taxed at a maximum rate of 7% in the canton of Vaud, depending on the family relationship, municipality, and amount involved. Note that the surviving spouse and registered partner are exempt from inheritance and donation taxes.

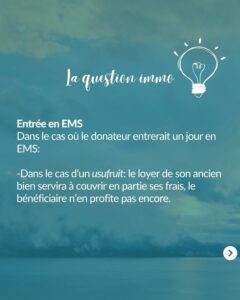

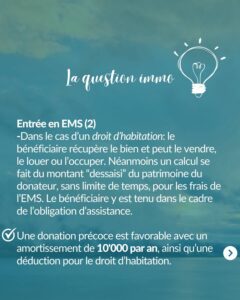

When calculating eligibility for supplementary benefits after moving into a nursing home (EMS), the donated amount is added back to the donor’s assets, regardless of when the donation occurred. However, an annual amortization of CHF 10,000 is applied. The beneficiary relative must contribute to the nursing home costs as part of their legal duty of support, but with deductions based on usufruct rights and amortization. Additionally, the nursing home resident can request an annual asset adjustment from the AVS office so that the extra CHF 10,000 deduction is taken into account.

Selling to one of your children can be complex, as it must generally be done at or near market value. The land registry informs the tax authorities, who may review transactions completed at significantly below-market prices and reclassify them as mixed donations. In such cases, the transaction is subject to donation tax in addition to transfer duties for the buyer and possibly capital gains tax for the seller.

If none of your relatives are interested in taking over the property, we do not recommend a life annuity sale, as the sums received are usually insufficient and the emotional burden can be considerable.

Instead, we recommend a standard sale to a third party at market value — allowing you to comfortably relocate and even make donations if you wish.

KasaMea Immobilier — by your side in life’s key moments!